Going into 2021, there is an anticipation that copper market will face the tightest market conditions in a decade owing to a substantial deficit. The forecasts predict 232 to 432 ktons of deficit in refined copper for this year.

May 6, 2021

The Copper Market, Treatment and Refining Charges

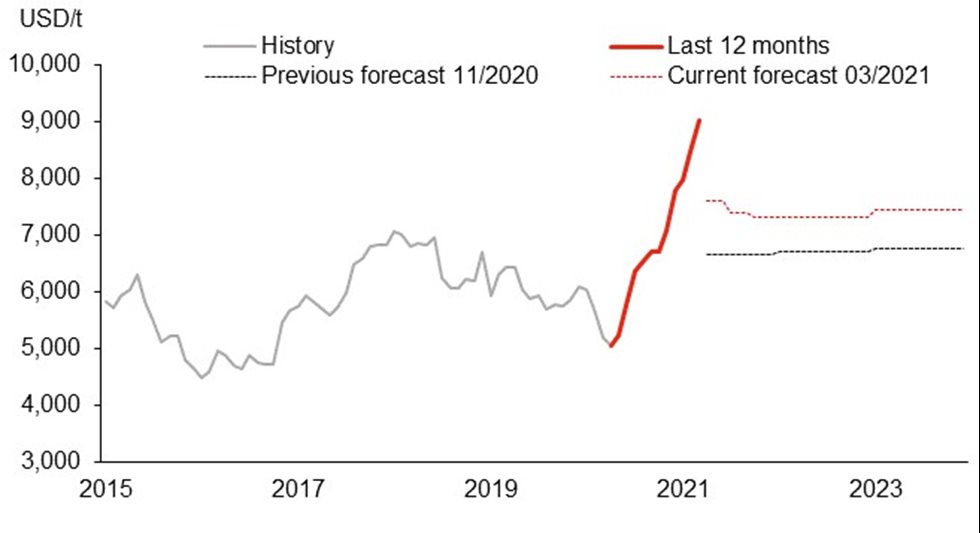

Despite all the uncertainty in 2020 caused by the pandemic, copper prices have ended 2020 at an eight years’ high, trading above 7 500 USD/t in London Metal Exchange. Since then, copper price forecasts were continuously revised upwards, driven by expectations of deficit and demand rebound.

LME-Copper Grade A Price, USD/t. Source: S&P Global Market Intelligence. Average spot prices for March as of 17.3.2021. Forecasts as of 11.03.2021

One of the copper price drivers during 2020 was the supply disruptions. Flows of metals concentrates from South American producer nations (such as Chile and Peru) have been disrupted by COVID restrictions. Overall mined production in 2020 decreased by 4%, according to S&P Global.

According to Goldman Sachs, the latest export data in 2021 from Chile and Peru showed sharp year on year declines in overall cathode exports and particularly to exports to China. Export declines could be an indication of weak trend in production in the end of 2020 and other disruptions. Firstly, Latin American mine supply has been restrained by weather-related logistical challenges in Chile affecting port operations in January. Secondly, strike action in Peru at the Las Bambas mine led MMG to halting operations in November 2020 to mid-January, Glencore suspended operations at Antapaccay in Peru because members of the local community blockaded the copper mine, and workers at Antofagasta’s Los Pelambres were involved in mediation process with the company. Thirdly, although there is no evidence of an impact on mine operations from COVID-19 related restrictions in South America, this could remain a restraining factor on the pace of production ramp-up.

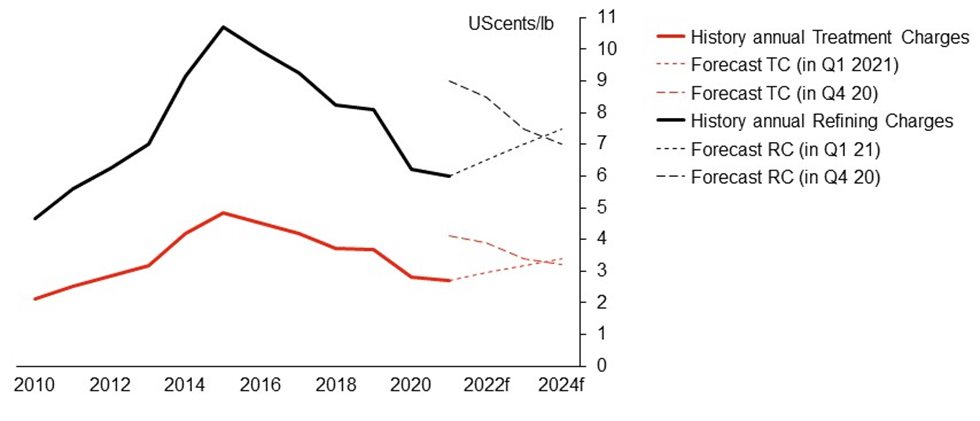

Treatment and Refining Charges

Although supply tightness was supportive for copper prices, smelters profits at the same time were put under pressure. Treatment and Refining Charges (TC/RCs) are the fees paid to smelters by mines for converting copper concentrate to copper cathode and key revenue source for smelters. Falling TCs are putting pressure on companies relying on external concentrate supplies.

The annual copper smelter benchmark Treatment Charges fell to the lowest level since 2012 to 59.5 USD per ton for year 2021. This is a strong indication of the concentrate market tightness. In the early months of 2021, spot Treatment and Refining charges for copper have continued to decline and are at their lowest level since 2012. In early March, according to Fastmarkets, the average spot treatment charge for clean concentrate fell to 38 USD per ton, signaling no improvement in supply conditions since November 2020 when the annual benchmark charges for 2021 were set.

The tightness in the copper concentrate market is anticipated to persist in the first half of the year at least, putting the pressure on smelters. Though, there is an expectation of recovery in global mine supply in the second half of 2021 and with that also an increase in spot Treatment Charges, supply disruptions are still possible. Multiple workers’ unions contract negotiations are expected to be taking place during this year with probability of potential strike actions in South America.

Treatment and Refining Charges (cif Shanghai) annual contracts and forecast. Source: S&P Global Market Intelligence

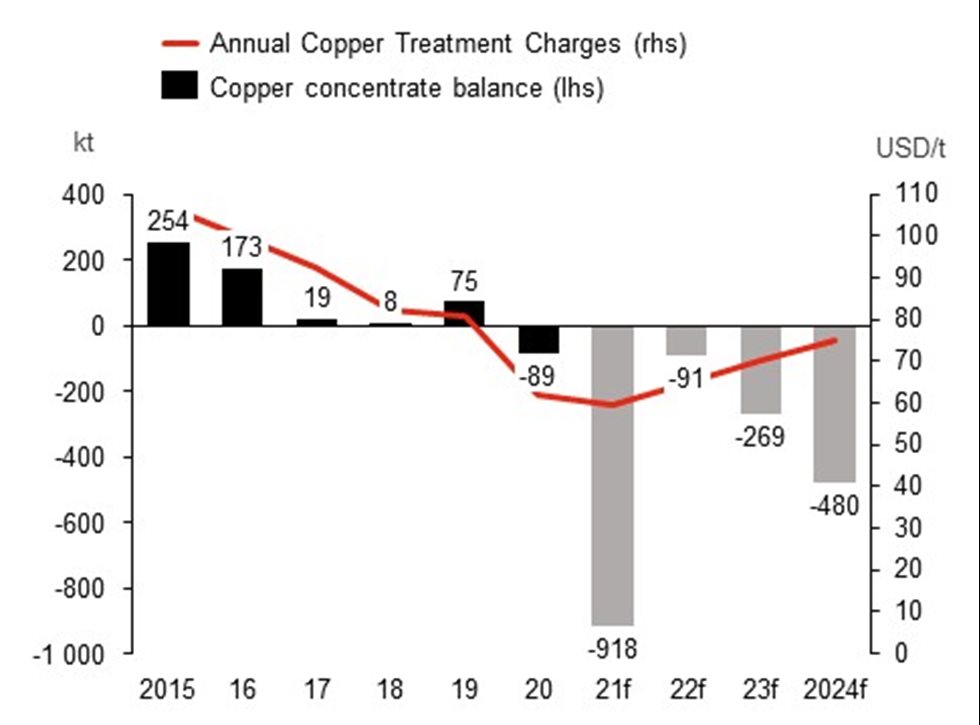

The current copper price of above 9 000 USD/t is seen as encouraging miners to boost output. Copper mine production is forecasted to rise by 2..4% in 2021, and by further 7% in 2022 boosted by recovering supply at existing mines, expansions and new capacity in Indonesia (Grasberg Block Cave mine ramp-up) , Peru (the startup of Mina Justa and the expansion of Toromocho) and Chile (Spence mine expansion). Mine production growth is expected to be tilted towards the second half of the year, conditional to diminishing risks in disruptions due to COVID-19. As annual benchmark copper Treatment Charge price is going to be set in the end of 2021, the expectation is that concentrate market tightness would relax until then. S&P Global forecasts rising annual benchmark Treatment Charges from 2022 onwards.

Copper concentrate balance and benchmark annual Treatment Charges. Source: S&P Global Market Intelligence

Global supply and demand

Shuttering of major economies in 2020 saw a -3.5% decrease in global GDP year over year according to International Monetary Fund (IMF). IMF expects global economy to grow 5.5% in 2021 conditional to successful vaccination campaigns and policy support in few large economies. Industrial commodities such as copper should be supported from recovery in economic activity and from economic stimulus packages such as infrastructure spending and stimulus plans.

China's GDP grew by an estimated 2.3% in 2020, being one of the few nations to post growth and the primary driver of the copper price recovery following the March 2020 crash. Chinese GDP is forecasted to increase by 8.1% in 2021 and be one of the key drivers for the demand of copper. Outside China, demand will ramp up as vaccinations roll out and stimulus packages continue to be implemented. Delays in the vaccination program schedules in many countries, however, could still push the bulk of the recovery into the second half of 2021.

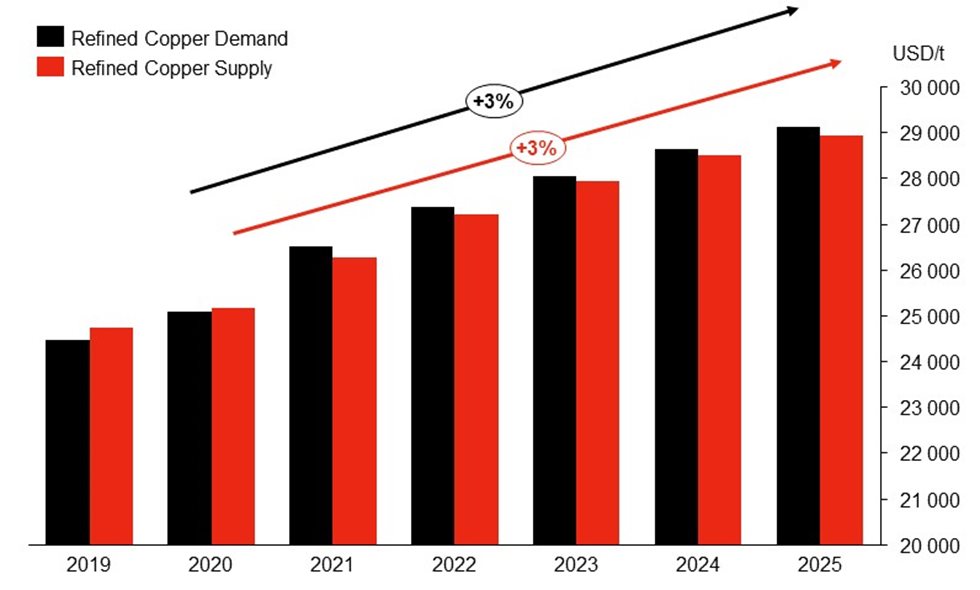

Refined copper demand and supply. Source: S&P Global Market Intelligence

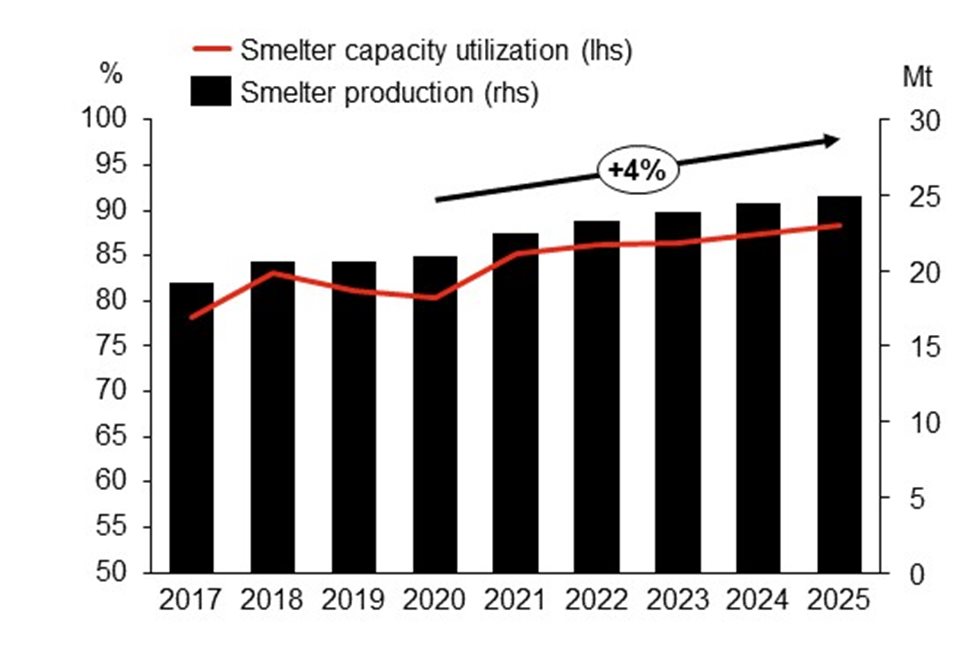

Copper demand is expected to be strongly boosted by the strong shift in global agenda towards sustainable growth. Focus on green or clean energy is expected during President’s Biden term with US rejoining Paris Agreement. China has indicated plans to become carbon neutral by the year 2060. Europe has raised the bar for decarbonization ambitions from 40 to 55% until 2030. Ambitious commitments would likely require large electrification efforts in transport, expanding renewable generation capacity and electrical networks with copper being an integral part of these developments. Green agenda is expected to provide strong tailwind for copper demand during this and upcoming years. Refined copper demand is expected to grow at 3% CAGR between 2020 and 2025. At the same time, smelter capacity utilization is expected to progressively increase to 85 - 88% in the coming 5 years in comparison to the 78..83% seen in last 5 years, catering strong demand for copper.

Historical and forecasted smelter production and smelter capacity utilization. Source: S&P Global Market Intelligence

On the other hand, peak mined copper supply appears to be fast approaching. Higher copper prices today should incentivize new supply investment to prevent what is currently a path to scarcity conditions by mid-decade.

Smelters continue to invest in upgrades and modernizations to secure margins

Prolonged low environment TC/RC environment might put some smelters in a challenging financial position. But it could also encourage others to continue investing in improving processes and strengthening technical capabilities. Smelters continuously strive to improve their position on the cost cuThe rve and become more competitive – the focus remains on upgrades and modernizations as well as process improvements to increase recovery. The sustainability agenda in turn demands adoption of solutions to reduce the emissions from smelters.

Contact local sales experts

Your information is safe. Check our privacy notice for more details.

Thank you!

We will shortly contact you. You can send a new inquiry again after 15 minutes.